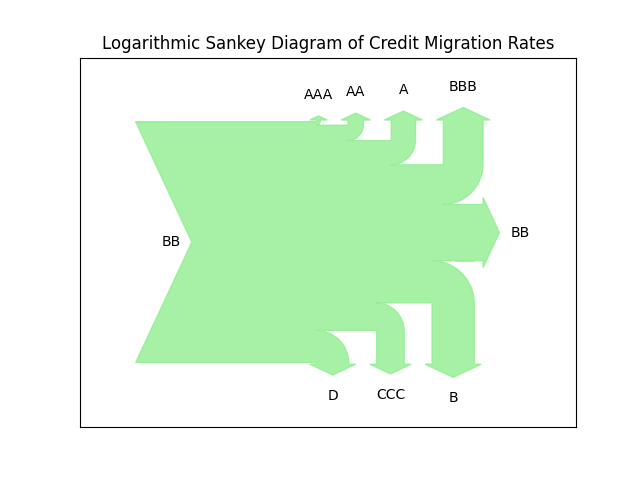

Sankey diagrams are very useful for the visualization of flows, especially when there is a conserved quantity. They can be tricky when some of the flows are much smaller than others. In the latest release of transitionMatrix we include an example of a log-scale version of Sankey

Using Sankey Diagrams Sankey Diagrams are a type of flow diagram composed of interconnected arrows. The width of the arrows is proportional to the flow rate. Sankey diagrams are often used in physical sciences (physics, chemistry, biology) and engineering but also in economics. They can be used to represent the relative role and significance of various inputs and outputs in a given process.

Sankey diagrams emphasize the major transfers within a system.

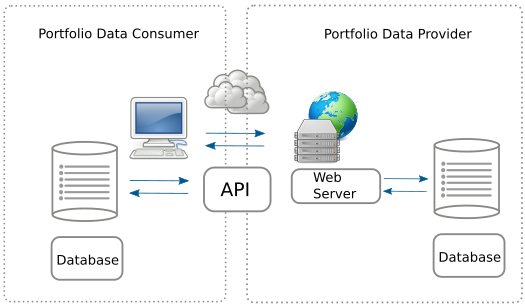

The 0.2 release of openNPL exposes a RESTful API that provides easy standardized online access to NPL credit portfolio data conforming to the EBA NPL templates

openNPL 0.2 release The open source openNPL platform supports the management of standardized credit portfolio data for non-performing loans. In this respect it implements the detailed European Banking Authority NPL loan templates. openNPL aims to be at the same time easy to integrate in human workflows (using a familiar web interface) and integrate into automated (computer driven) workflows.

The latest (0.2) release exposes a REST API that offers machine oriented access using, what is by now, the most established mechanism for achieving flexible online data transfers.

In the Back-to-School for 2020 we have more ways to access the Academy, new functionalities and more courses. In the rest of this post you will find a summary of the changes with pointers to further information where required

Risk Management will not be the same going forward: too much is at stake The summer is over in the Northern Hemisphere - and what an unusual summer has it been! Worldwide the implications and challenges of adjusting to a Covid-19 pandemic are still a major issue, affecting individuals, companies and governments.

At Open Risk we have been tracking and will continue to interpret the impact of the pandemic via a number of projects:

openNPL now Available in Dockerized Form Following up on the first release of openNPL the platform is now available to install using Docker. Running openNPL via docker is the installation option that simplifies the manual process (but a working docker installation is required!).

Docker Hub You can pull the latest openNPL image from Docker Hub (This method is recommended if you do not want to mess with the source distribution).

Non-Performing Loans The covid-19 crisis will certainly impact the concentration of Non-Performing Loans but given the special nature of this economic crisis compared (in particular) with the 2008 financial crisis it is unclear how precisely things will evolve.

In a previous post and white paper (OpenRiskWP07_022616) we discussed the importance of advancing open and transparent methodologies for managing the risks associated with such credit portfolios. Effective management of NPL is also a top regulatory priority.

The community mobility reports and OpenCPM In a previous post we introduced new OpenCPM functionality that integrates COVID-19 community mobility data (currently from Google). The reports chart movement trends over time by geography, across different categories of places such as retail and recreation, groceries and pharmacies, parks, transit stations, workplaces, and residential.

While these reports are unlikely to persist as open data sources in the long term, the current availability (as of May 2020) enables providing within OpenCPM a mobility data dashboard that can help draw insights through visualization and statistical analysis.

The community mobility reports and OpenCPM As the COVID-19 pandemic unfolded technology providers (most notably Google and Apple) made available to the public aggregated and anonymized data about human mobility in the crisis period (on the basis of smartphone location data). These Community Mobility Reports provide insights into how mobility patterns changed in response both to pandemic news and policies aimed at combating COVID-19.

The reports chart movement trends over time by geography, across different categories of locations and activities, such as retail and recreation, groceries and pharmacies, parks, transit stations, workplaces, and residential.

Course Content This course is a CrashProgram (short course) introducing the GeoJSON specification for the encoding of geospatial features. The course is at an introductory technical level. It requires some familiarity with data specifications such as JSON and a very basic knowledge of Python

Who Is This Course For The course is useful to:

Any developer or data scientist that wants to work with geospatial features encoded in the geojson format How Does The Course Help Mastering the course content provides background knowledge towards the following activities:

Course Content This course is an introduction to the concept of credit contagion. It covers the following topics:

Contagion Risk Overview and Definition Various Contagion Types and Modelling Challenges The Simple Contagion Model by Davis and Lo Supply Chains Contagion Sovereign Contagion Who Is This Course For The course is useful to:

Risk Analysts across the financial industry and beyond Risk Management students Quantitative Risk Managers developing or validating risk models How Does The Course Help Mastering the course content provides background knowledge towards the following activities:

Making Open Risk Data easier In an earlier blog post we discussed the promise of Open Risk Data and how the widespread availability of good information that is relevant for risk management can substantially help mitigate diverse risks.

The list of Open Risk Data providers, particularly from public sector, keeps increasing and we are aiming to document all available datasets in the dedicated page of the Open Risk Manual.

The trailblazing Wikidata project In this post we want to introduce another facility, an online database that allows the (relatively) easy publication of structured risk data.

Semantic Web Technologies The Risk Model Ontology is a framework that aims to represent and categorize knowledge about risk models using semantic web information technologies.

In principle any semantic technology can be the starting point for a risk model ontology. The Open Risk Manual adopts the W3C’s Web Ontology Language (OWL). OWL is a Semantic Web language designed to represent rich and complex knowledge about things, groups of things, and relations between things.

The motivation for federated credit risk models Federated learning is a machine learning technique that is receiving increased attention in diverse data driven application domains that have data privacy concerns. The essence of the concept is to train algorithms across decentralized servers, each holding their own local data samples, hence without the need to exchange potentially sensitive information. The construction of a common model is achieved through the exchange of derived data (gradients, parameters, weights etc).

We introduce a side-by-side review of the main open source ecosystems supporting the Data Science domain: Julia, Python, R, the trio sometimes abbreviated as Jupyter

Overview of the Julia-Python-R Universe A new Open Risk Manual entry offers a side-by-side review of the main open source ecosystems supporting the Data Science domain: Julia, Python, R, sometimes abbreviated as Jupyter.

Motivation A large component of Quantitative Risk Management relies on data processing and quantitative tools (aka Data Science ). In recent years open source software targeting Data Science finds increased adoption in diverse applications. The overview of the Julia-Python-R Universe article is a side by side comparison of a wide range of aspects of Python, Julia and R language ecosystems.

Data Quality and Exploratory Data Analysis using Python In two new Open Risk Academy courses we figure step by step how to use python to work to review risk data from a data quality perspective and how to perform exploratory data analysis with pandas, seaborn and statsmodels:

Introduction to Risk Data Review Exploratory Data Analysis using Pandas, Seaborn and Statsmodels

Open Source Securitisation Motivation After the Great Financial Crisis securitisation has become the poster child of a financial product exhibiting complexity and opaqueness. The issues and lessons learned post-crisis were many, involving all aspects of the securitisation process, from the nature and quality of the underlying assets, the incentives of the various agents involved and the ability of investors to analyze the products they invested in. While the most egregious complications involved various types of re-securitisation and/or the interplay of structured credit derivatives undoubtedly even vanilla securitisation structure has a considerable amount of business logic.

Visualization of large scale economic data sets Economic data are increasingly being aggregated and disseminated by Statistics Agencies and Central Banks using modern API’s (application programming interfaces) which enable unprecedented accessibility to wider audiences. In turn the availability of relevant information enables more informed decision-making by a variety of actors in both public and private sectors. An excellent example of such a modern facility is the European Central Bank’s Statistical Data Warehouse (SDW), an online economic data repository that provides features to access, find, compare, download and share the ECB’s published statistical information.

ESMA Securitisation Templates are now documented at the Open Risk Manual The ESMA Securitisation Templates are now fully documented at the Open Risk Manual. Users can browse, search and cross-reference with the rest of the knowledge base.

Category Browsing The ESMA Templates Categories are part of both the Securitisation category and the Information Technology Category. Each one of the templates and each one of the sections within a template forms its own category.

The challenge with historical credit data Historical credit data are vital for a host of credit portfolio management activities: Starting with assessment of the performance of different types of credits and all the way to the construction of sophisticated credit risk models. Such is the importance of data inputs that for risk models impacting significant decision-making / external reporting there are even prescribed minimum requirements for the type and quality of necessary historical credit data.

Release of version 0.4.1 of the transitionMatrix package focuses on stressing transition matrices Further building the open source OpenCPM toolkit this realease of transitionMatrix features:

Feature: Added functionality for conditioning multi-period transition matrices Training: Example calculation and visualization of conditional matrices Datasets: State space description and CGS mappings for top-6 credit rating agencies Conditional Transition Probabilities The calculation of conditional transition probabilities given an empirical transition matrix is a highly non-trivial task involving many modelling assumptions.

Release of version 0.4 of the transitionMatrix package Further building the open source OpenCPM toolkit this realease of transitionMatrix features:

Feature: Added Aalen-Johansen Duration Estimator Documentation: Major overhaul of documentation, now targeting ReadTheDocs distribution Training: Streamlining of all examples Installation: Pypi and wheel installation options Datasets: Synthetic Datasets in long format Enjoy!